Breaking Down the American Medical Bill

English

One of the great pleasures of living abroad is experiencing another country's social systems firsthand — even when that experience is brutal. Having gone through surgery in America, a country where you regularly hear about people going bankrupt from enormous medical bills, I feel qualified to walk you through how American healthcare billing actually works. Let's go. This one's long.

Rewind about a month: a CT scan confirmed surgery was necessary. I had insurance, but the fear of receiving an astronomical bill was very real. I asked ChatGPT what to watch out for, and the answer was clear: confirm that every single medical service provider is in your insurance network. Apparently, it's entirely possible for just the anesthesiologist to be out-of-network, triggering a massive surprise bill.

That phrase — every single medical service provider — is the key. Unlike Japan, where the hospital sends you one bill that covers everything, America operates on a highly specialized division of labor. A single surgery involves the hospital facility, the surgeon, the anesthesiologist, the radiologist, and more — each of whom bills you separately. That's exactly how you end up with a situation where only your anesthesiologist is out-of-network.

Next, you need to understand two concepts: Billed and Allowed. Billed is the sticker price set by the hospital — a number that's essentially meaningless unless you're uninsured or out-of-network. What actually matters is Allowed, the price negotiated between the provider and your insurer. Let me make this concrete with my own heel reconstruction surgery.

Brace yourself: the Billed amount for the hospital facility alone was $77,000. With insurance, that gets compressed to an Allowed amount of $14,000. Each medical procedure also has a CPT code, and for each code the patient's share and the insurance's share are defined. After all that, my out-of-pocket came to $8,000 — roughly one-tenth of the sticker price.

Note that this is the hospital facility fee only. Separate bills come from each doctor. Each provider negotiates its own Billed/Allowed rates with your insurer, and each CPT code carries its own patient/insurance split. Multiply this across every party involved and your head starts spinning. There's also a detail called Modifiers: the lead surgeon and the assistant surgeon may bill the same CPT code at very different Allowed rates.

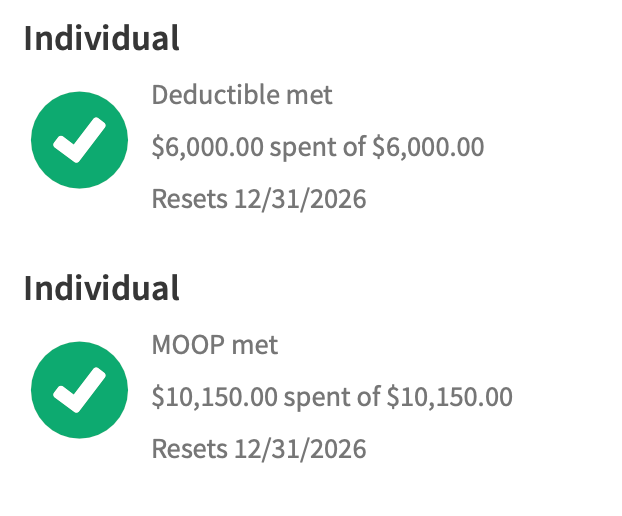

The next thing to understand is how insurance itself works. It runs in three phases. First is the Deductible — the amount you pay entirely out of pocket before insurance contributes anything. Then comes Coinsurance, where you and the insurer split costs. Finally there's the Out-of-Pocket (OOP) Maximum: once you hit that ceiling, insurance covers 100%. My plan has a $6,000 Deductible and a $10,150 OOP Max. Behold the glorious screenshot of me hitting that OOP Max. The green checkmark is not the comfort they think it is.

As long as you stay in-network, the OOP Max means you won't go bankrupt — expensive, but not ruinous. That's why staying in-network is the single most important thing. Plans with lower Deductibles and OOP Maxes exist, but they come with higher monthly premiums. Since I've been healthy, I'd chosen a plan with the highest possible Deductible and OOP Max in exchange for lower monthly payments. Great plan. Incredible timing.

This whole structure exists for one simple reason: the US has no unified pricing rules for medical care. Hospitals and doctors set their own prices freely, and the actual price is determined through individual contracts with insurers. The inflated Billed price exists to handle uninsured and out-of-network cases and to anchor those negotiations. That dual-price structure is what makes this system look so bizarre from the outside.

The insurer's negotiating leverage depends on patient volume — a large insurer that sends many patients has more power over providers. Conversely, a hospital or physician with a strong enough brand can attract patients on their own, reducing their incentive to lower Allowed rates. Ah... capitalism.

There is an exception: some organizations integrate insurance and healthcare delivery under one roof, eliminating price negotiation entirely. It's a designed world somewhat reminiscent of Japan's system — you won't get a surprise bill after your visit. But this model doesn't seem particularly popular in the US.

The result: I now cross-reference the Explanation of Benefits my insurer sends — a summary of what I actually owe — against waves of individual bills arriving from the hospital, each surgeon, and everyone else. Claude Code handles the reconciliation with impressive accuracy these days, which helps. It's still a pain.

One last thing not to overlook: price negotiation. Patients can negotiate directly with providers — essentially asking for a discount in exchange for paying in full upfront. This is completely separate from OOP Max. Fascinating. Those negotiations are still ahead of me. Wish me luck.

To bring it back to where I started: I paid roughly $10,000 and spent two months unable to walk for the privilege of this firsthand education in the American healthcare system. Whether that's expensive or cheap, I honestly can't tell — though I'm pretty sure it's expensive. My experience points are a little higher now. If you feel sorry for me, buying me a book would be appreciated.

日本語 {#japanese}

異国で生活する醍醐味の一つとして、そこの国の社会制度や仕組みを体験できることにある。それが酷い体験であったとしてもだ。数千万円クラスの高額請求を受けて破産したと言うニュースをよく聞くアメリカで、手術をした私はアメリカの医療制度を解説できる立場にあると思う。さあ、解説、行ってみましょう!長いぞ!

時を遡ること1ヶ月、CTをとった結果、手術が確定した。もちろん保険は入っているが、とてつもない高額請求を受けるのではないかと言う恐怖があった。ChatGPTに何に注意すべきか聞いてみると、すべての医療サービス提供者が、自分の保険のネットワーク内であるかどうか確認が必要だ!という。例えば、麻酔医がだけが保険のネットワーク外で高額請求になることがあるらしい。

そう、ここでいう、すべての医療サービス提供者、が重要である。日本のように病院に聞けばまとめて1本の請求が来る、ということはない。アメリカは高度な分業社会、1回の手術でも病院、外科医、麻酔医、放射線医など複数の主体が関与し、それから別々に請求が来る。だから、麻酔医だけネットワーク外と言うことがありえてしまうのである。

それから、BilledとAllowedという概念を理解しておく必要がある。Billedとは病院が出す定価であり、保険がない人・もしくはネットワーク外でないかぎり意味のない数字である。実際に意味を持つのは、保険会社との契約によって決まるAllowedであり、これが実質的な価格になる。概念だけでわかりにくいと思うので、私の踵骨修復手術の例を取って説明してみたい。

心を落ち着けて聞いて欲しいが、この手術の病院からのBilled(定価)は77,000ドルである。日本円に直すと1200万円である。だんだん想像ついてきただろうか。建設現場で働いている人が高いところから落ちて踵を骨折。保険がなく、この金額を払うことができずに、社会から落伍してしまうことが。しかも、踵の骨折は手術しないと歩けなくなるのである。医療が全員に提供される日本がいかに素晴らしい国かわかる。医療行為に資本主義を適応するというのはこういうことだ。

保険がある私の場合は、Allowed(保険会社が交渉した後の値段)は14,000ドルまで圧縮される。そして、実施した医療行為ごとにCPTコードというのが発行されており、そのCPTコードごとに、患者が払う金額と保険が払う金額が決められている。結果、私が支払う金額は、8000ドルまで圧縮される。Billedの1/10になった。

ご注意いただきたいのは、これは病院の施設使用料のみで、医者からは別の請求が来る。医者と保険会社の交渉が行われ、Billed/Allowedが決まり、CPTコードごとに患者と保険の支払い割合が決まることになる。これをすべての医療主体と保険がおこなっていると思うと、複雑さに頭がクラクラする。そして、細かい話だが、CPTコード以外に、Modifierがあり、例えば主執刀医と助手では同じCPTコードでもAllowedが全然違ったりする。

次に理解しないといけないポイントが保険の仕組みだ。これは3つのフェーズに分かれている。最初はDeductibleと呼ばれており、まず自分で支払う金額である。その後は、Coinsuranceと呼ばれ、保険と分担して支払う。最終的にはOut of Pocket(OOP) Maxと呼ばれる金額が設定されており、それ以上は保険が全額負担する。僕の保険の場合は、Deductibleが、6000ドルで、OoP Max が 10,150ドルである。みよ、このOoP Maxに到達した神々しいスクリーンショットを。グリーンのチェックマークつけられても困る。

OoP Maxまでしか払わなくて良いので、ネットワーク内であれば安くはないが破産することはない。だから、ネットワーク内で医療行為を受けることが何よりも重要である。また、同じ保険会社でDeductibleやOoP Maxが少ない商品もあるが、毎月の支払いが大きくなる。私は今のところ健康体なので、DeductibleやOoP Maxが最大の代わりに毎月の支払いが少ない保険を選んでいたのである。

このような構造になっている理由は単純で、アメリカには医療価格の統一ルールが存在しないからである。病院や医者は自由に価格を設定し、保険会社と個別に契約することで実際の価格が決まる。無保険やネットワーク外のケースに対応し、保険会社との交渉のためにBilledという高い価格が維持される。この二重価格構造が外から見たときの異常さを生んでいる。

保険会社と医療サービス提供者の交渉には様々な要素がある。たくさんの患者を送客できる保険は病院や医者に対して強い交渉力を持つ。逆に、ブランド化した病院や医師の場合、自分で集客できてしまうので、Allowedを下げる意味が薄れてくる。あぁ。。。資本主義である。

例外的に保険会社と医療提供が一体化したサービス提供者も存在する。そもそも価格交渉をする必要がない。ある意味日本に近い、設計された世界が実現する。もちろんその保険の病院にしかいくことができないのでそこは不便だが、病院に行ってみて想定外の請求を受けるみたいなことはなくなる。ただ、この形式はアメリカではあまり人気がないように思う。

結果、私は保険会社から送られてくるExplanation of Benefits、要は自分がいくら支払わないといけないかまとめた書類と、病院や医者などから五月雨式に来る請求書を突き合わせて確認することになるのである。もちろん最近はClaude Codeが精度高くやってくれるから楽ではあるが、とても面倒臭い。

そして最後に忘れてはならないのが、価格交渉である。患者と医療サービス提供者間では価格交渉が成立する。要は一括で払うから、値引きしてください、みたいな話だ。これはOoP Maxとは全く関係ない。面白すぎる!交渉はこれから。僕の幸運を祈っておいてください。

最初の話に戻るが、私はこのシステムを体験するというエンタメに2ヶ月歩けない怪我を負って10,000ドル、150万円支払った。高いか安いかわからないというか絶対高いに違いないが、また私の経験値が少し増えた気がする。不憫に思う方はこちらから暇つぶしに読む本代でもお願いします!